Get Dr 1083 Colorado Form

Get Dr 1083 Colorado Form

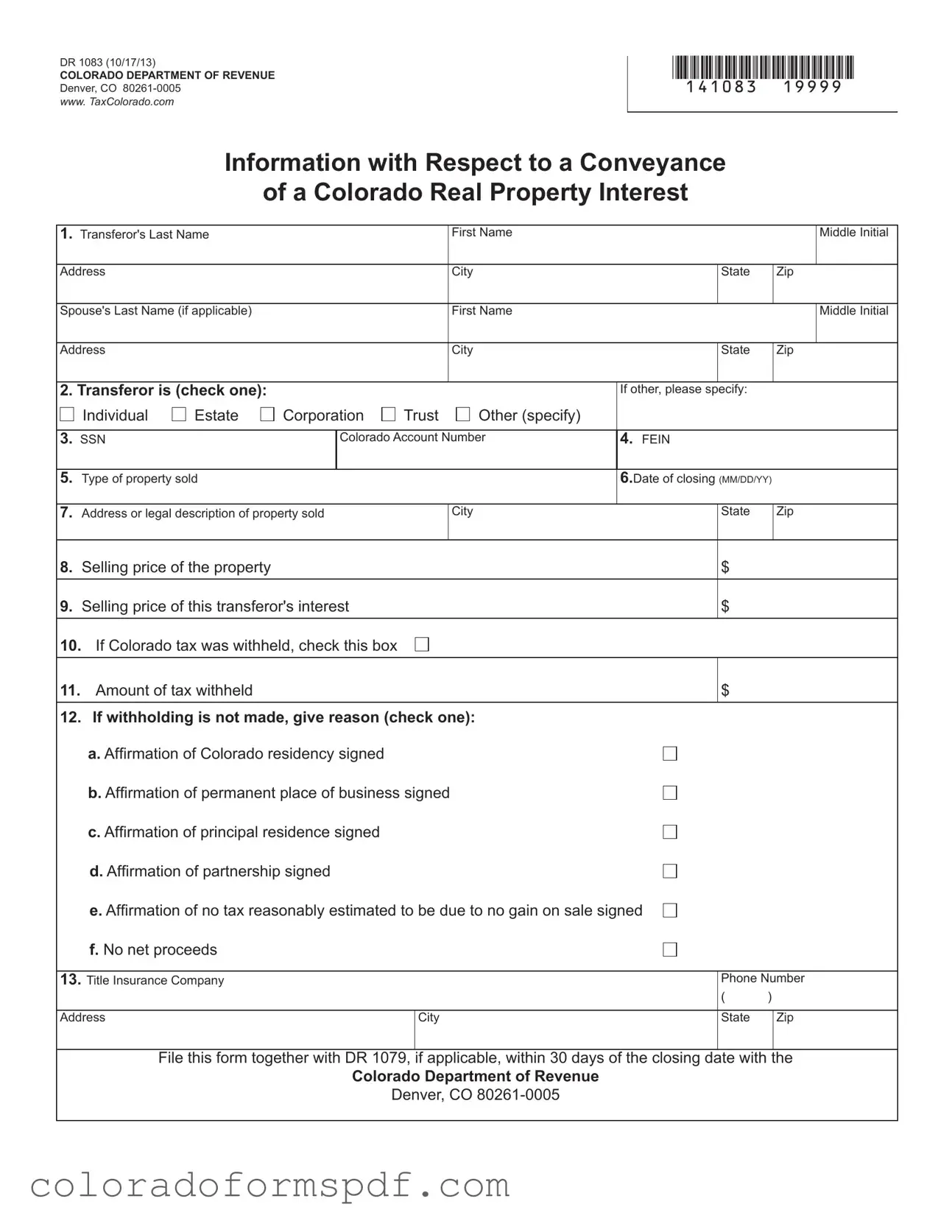

The DR 1083 form, issued by the Colorado Department of Revenue, plays a crucial role in the transfer of real property interests within the state. This form is specifically designed to gather essential information regarding the conveyance of real estate, ensuring compliance with Colorado tax regulations. Key details required on the form include the names and addresses of the transferors, the type of property being sold, and the selling price. Additionally, it addresses the withholding tax obligations for non-residents, which applies to sales valued at $100,000 or more. The form also contains sections for affirmations related to residency and business operations, allowing transferors to clarify their tax status. If applicable, the form must be filed within 30 days of the closing date, alongside the DR 1079 form if tax withholding has occurred. Understanding the requirements of the DR 1083 is essential for anyone involved in real estate transactions in Colorado, as it ensures that all parties adhere to state tax laws and avoid potential penalties.

When filling out and using the DR 1083 form in Colorado, there are several important points to keep in mind:

Understanding these key points can help ensure compliance with Colorado tax regulations related to real property transactions.

Colorado Child Support Modification Form - The court will review your submission and may require a hearing, depending on the situation.

Having the correct paperwork is essential when conducting a tractor sale in Arizona, and the Arizona Tractor Bill of Sale form is a crucial part of this process. To ensure a smooth transaction and transfer of ownership, you may want to check out All Arizona Forms that assist in documenting this legal agreement securely.

Colorado Tax Exempt Certificate - Buyers should consult relevant state laws regarding exemptions.

When filling out the DR 1083 form for Colorado, there are several important dos and don'ts to keep in mind. Following these guidelines can help ensure that your submission is accurate and compliant with state regulations.

| Fact Name | Details |

|---|---|

| Form Purpose | The DR 1083 form is used to report the conveyance of a real property interest in Colorado. |

| Filing Requirement | This form must be filed within 30 days of the closing date if Colorado tax was withheld or would have been withheld. |

| Withholding Tax | A withholding tax applies to sales of Colorado real property valued at $100,000 or more, particularly for nonresidents. |

| Governing Law | The form is governed by §39-22-604.5, C.R.S., which outlines the withholding requirements for real property transfers. |

| Exceptions to Withholding | No withholding is required if the transferor is a Colorado resident or if the selling price is less than $100,000. |