Get Colorado Dr 0204 Form

Get Colorado Dr 0204 Form

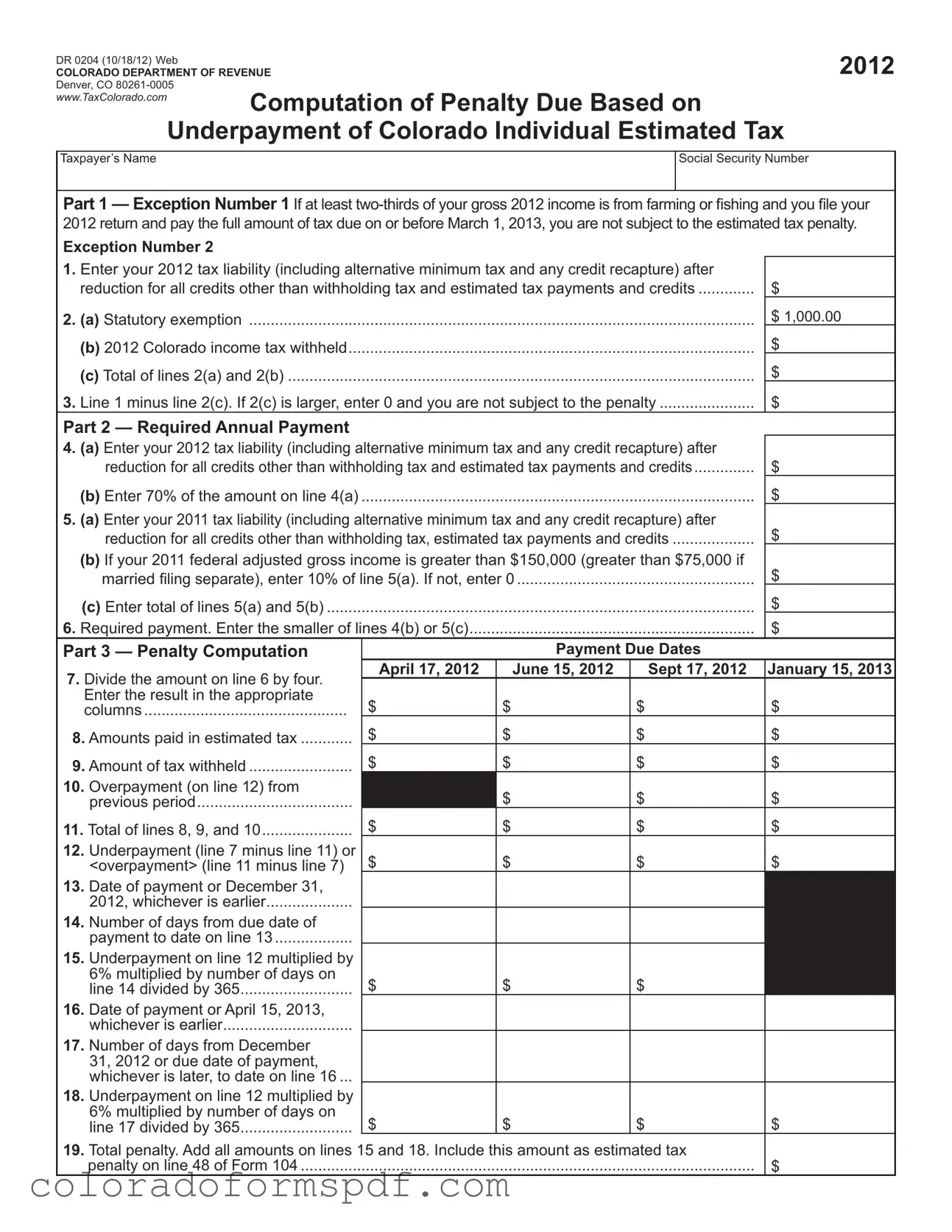

The Colorado DR 0204 form plays a crucial role for individuals who need to calculate their estimated tax penalties due to underpayment of taxes. This form is specifically designed for Colorado taxpayers and outlines the necessary steps to determine if a penalty applies based on their estimated tax payments. It includes sections that address exceptions for certain taxpayers, such as those whose income primarily comes from farming or fishing. Additionally, it details how to compute the required annual payment, which can be based on either the current year's tax liability or the previous year's tax liability, depending on specific criteria. The form also guides users through the penalty computation process, providing a clear method for calculating any penalties owed. Taxpayers must be diligent in filling out this form to ensure compliance and avoid unnecessary penalties. With its structured layout, the DR 0204 form helps taxpayers navigate the complexities of estimated tax payments while ensuring they fulfill their obligations to the Colorado Department of Revenue.

When filling out and using the Colorado DR 0204 form, it is essential to understand several key points to ensure compliance and avoid penalties. Here are the main takeaways:

Completing the DR 0204 form accurately and on time is crucial for avoiding unnecessary penalties. Stay informed and proactive in your tax planning to ensure compliance with Colorado tax regulations.

Dr0104cr - Consider the impact of military service on your residency status.

The Arizona Operating Agreement form is a crucial document for limited liability companies (LLCs) operating in Arizona. This form outlines the management structure, operational guidelines, and member responsibilities within the company. For further information, you can refer to the Operating Agreement form. Having a well-drafted Operating Agreement can help prevent misunderstandings and ensure smooth business operations.

Colorado Child Tax Credit 2023 - It helps ensure that donations are applied correctly towards qualifying child care programs.

Wholesale License Colorado - The DR 0172 form helps manage tax exemptions for the construction industry.

When filling out the Colorado DR 0204 form, there are several important guidelines to follow to ensure accuracy and compliance. Here is a list of things you should and shouldn't do:

| Fact Name | Details |

|---|---|

| Form Title | Computation of Penalty Due Based on Underpayment of Colorado Individual Estimated Tax |

| Governing Law | Colorado Revised Statutes, Title 39, Article 22 |

| Filing Deadline | Taxpayers must file their 2012 return and pay by March 1, 2013, to avoid penalties if exceptions apply. |

| Exceptions to Penalty | Penalties are waived if two-thirds of income is from farming or fishing, and taxes are paid on time. |

| Annual Payment Calculation | The required annual payment is the lesser of 70% of the current year's tax or 100% of the previous year's tax liability. |

| Penalty Computation | Penalties are calculated based on underpayment amounts and the number of days overdue, using a 6% rate. |

| Annualized Installment Method | Taxpayers with uneven income can use this method to calculate estimated tax payments based on income received. |